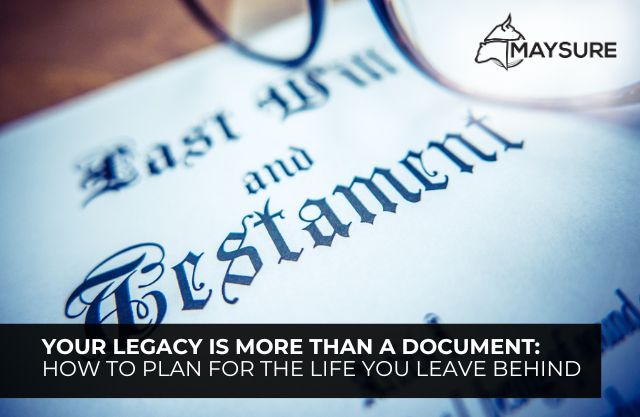

Your Legacy Is More Than a Document: How to Plan for the Life You Leave Behind

When most people think of legacy planning, they imagine paperwork, legal jargon, and technical terms like “wills” and “testamentary trusts.” But at its heart, legacy planning is about love, values, and protecting the people you care about. It’s a reflection of how you want to be remembered and the impact you hope to leave behind.

At Maysure Financial Services, we believe your legacy should be intentional, personal, and aligned with your values, not just your assets.

What Is Legacy Planning?

Legacy planning goes beyond drafting a will. It’s a comprehensive process that includes:

- Wills and estate planning

- Trusts and guardianship decisions

- Succession planning for businesses

- Tax-efficient transfer of wealth

- Long-term protection for your family’s financial future

While these tools are essential, the heart of legacy planning lies in asking:

What do I want to leave behind, and for whom?

Why Legacy Planning Is Important in South Africa

In South Africa, many families assume their estates will automatically pass to their loved ones, but this isn’t always the case. Without a clear, up-to-date will and proper estate structure, you could leave your family vulnerable to legal complications, delays, and unnecessary financial stress.

According to the Master of the High Court, over 70% of South Africans pass away without a valid will, which can result in the state deciding how your estate is distributed. A well-considered legacy plan ensures:

- Your wishes are honoured

- Your loved ones are protected

- Your estate is managed efficiently

- Your legacy reflects the life you’ve built

When Should You Start Planning Your Legacy?

It’s never too early or too late to begin planning your legacy. Key life milestones that should trigger a review of your estate and financial plan include:

- Getting married or entering a life partnership

- Becoming a parent or legal guardian

- Starting or selling a business

- Receiving an inheritance or growing your wealth

- Buying property or other major assets

Your legacy plan should grow and adapt with your life. A will written five or ten years ago may no longer reflect your current relationships, priorities, or financial position.

Tools to Support Your Legacy

Maysure Financial Services helps you plan with both technical precision and personal care. Key tools we use in legacy planning include:

1. Wills

A valid, professionally drafted will ensures your estate is distributed according to your wishes and gives clarity to your loved ones.

2. Trusts

Setting up a trust can protect vulnerable beneficiaries (like minors or dependants with disabilities) and ensure assets are managed responsibly.

3. Life Cover for Estate Planning

Life insurance can be used to settle estate costs and provide liquidity, so your heirs don’t have to sell assets to cover debts or taxes.

4. Guardianship Provisions

If you have minor children, you can use your will to nominate legal guardians, giving you peace of mind that they’ll be cared for by someone you trust.

5. Business Succession Planning

If you’re a business owner, succession planning is vital to ensure your company continues operating smoothly and that your partners and family are not left in financial limbo.

Your Legacy Is a Living Plan

Legacy planning isn’t a once-off task—it’s a living process that evolves with your life. Reviewing your plan every 2–3 years ensures your will, insurance policies, and financial structures still reflect your goals and the people you want to protect.

At Maysure, we understand that your legacy is more than paperwork—it’s personal. That’s why we offer tailored guidance and long-term support to help you build a legacy that honours your life, protects your family, and preserves your values.

Start Your Legacy Planning with Maysure Financial Services

Whether you’re reviewing your will, planning for your children’s future, or preparing to transfer your business, our experienced team is here to guide you. We believe that protecting your legacy should feel empowering—not overwhelming.📞 Get in touch with Maysure today and take the first step in creating a legacy worth remembering.